My intention is for The Dispatch to provide a clear perspective on China’s digital economy and leading digital players.

There are already lots of stats, market updates, news reports, and stock analysis. The Dispatch won’t replicate these.

Instead, The Dispatch summaries and presents deep thinking on what’s happening in China’s digital economy and where things might be going next. It provides readers context and frameworks to think about ‘big picture’ issues like:

- What does digitalization of China’s services market look like?

- How do Chinese internet giants approach user acquisition and retention?

- Where do threats to current e-commerce business models exist?

- How unique are China’s internet platforms?

- Does social media have a common trajectory in China and the West?

The Dispatch won’t discuss the latest trends, new challenger platforms, or how to market your products in China. If you’re after that, you can follow my daily LinkedIn updates here or sign up to AgencyChina’s regular newsletter here.

Often, Chinese-language sources break key stories around 48-72 hours earlier than English-language counterparts.

But, aside from the time-lag, I don’t think there’s a substantive difference between what’s reported day-to-day:

Company X raises $Y billion, Firm B acquires Firm A, and Firm M announces a plan to launch some ridiculous number of automated convenience stores by year’s end.

Yes, individual article quality varies. But that’s a media reality, rather than an issue with English-language China tech coverage.

Where both English-language and Chinese-language sources arguably suffer is deep thinking about the internet, digitalization, and corporate strategy. Reporting on the day-to-day takes precedence to unpacking interesting questions like:

- Is the gap between BAT getting bigger or smaller?

- Why do Chinese tech giants tend to engage in a lot of non-core business activities?

- Does Meituan really need to have mobility solutions as part of its ecosystem?

This is the gap The Dispatch fills.

The Dispatch is currently in a pilot phase. I’ll release three articles to test the waters. If the pilot’s successful, The Dispatch will be offered as an annual subscription, with articles delivered fortnightly.

If this article’s been forwarded to you but you haven’t formally signed up for The Dispatch through LinkedIn, then you can do so here.

The Dispatch offers perspectives, frameworks and challenges which may be enjoyable, useful or provocative. The Dispatch’s perspectives, frameworks and challenges are a distillation of:

- Mental models I’m working on to understand and navigate China’s internet

- Mental models individual investors, investment houses and leading consultancies have used to analyze markets, competition, and digital disruption

- Conversations with movers-and-shakers from Alibaba, Tencent, Meituan, JD, Little Red Book, and Luckin’ Coffee

- Consulting assignments with digital economy incumbents and upstarts

- Comparative analysis of global digital ecosystems

- Voluminous compilation and analysis of leading Chinese founders, venture capitalists and public intellectuals’ reflections on China’s digital ecosystem

Image 1: Photograph from an interview I conducted with Meituan’s CMO in 2018

Aside from enjoyment and practical value, it’s my ultimate hope that The Dispatch’s perspectives, frameworks and challenges are taken, built upon and made better.

The Dispatch’s for three groups, which I anticipate will overlap or intersect:

- Folks interested in China’s digital economy

- Folks with a footprint in China’s digital ecosystem (noting the disclosure in the footnotes below)[1]

- Folks interested in internet, tech and all things digital

[1] The content here is for informational purposes only and should not be taken as legal, business, tax, or investment advice. It does not constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment.

1. China’s key digital players have pretty much run out of fast, cheap user growth

I. Various dividends that facilitated fast, cheap user growth are almost exhausted.

Between 2010 and 2015, the growth of China’s mobile internet benefited from lots of users coming online, spending more time online and companies having plenty of cash to build products and fight for more users. Three dividends played out simultaneously:

- Demographic Dividend

- Time on Device Dividend

- Capital Dividend

Now, these dividends are close to running out.

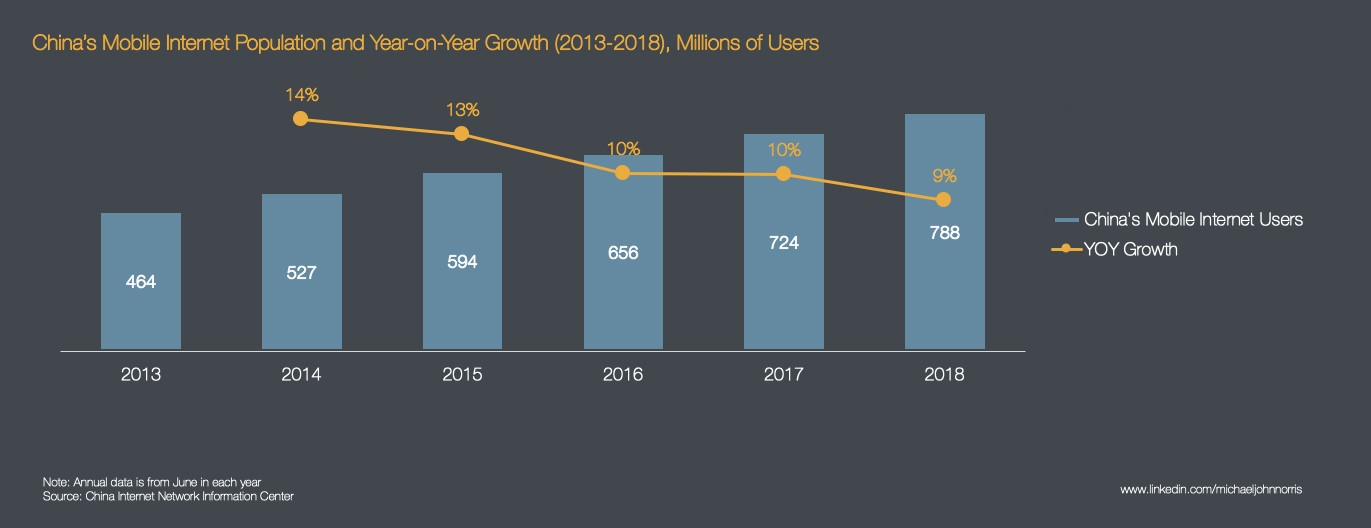

The demographic dividend is coming to an end. According to China’s Internet Network Information Center, China has over 770 million mobile internet users. With more users connected to the internet, year-on-year double-digit growth in mobile users has given way to single-digit growth.

Figure 1: Chinese Mobile Internet Users and Year-on-Year Growth

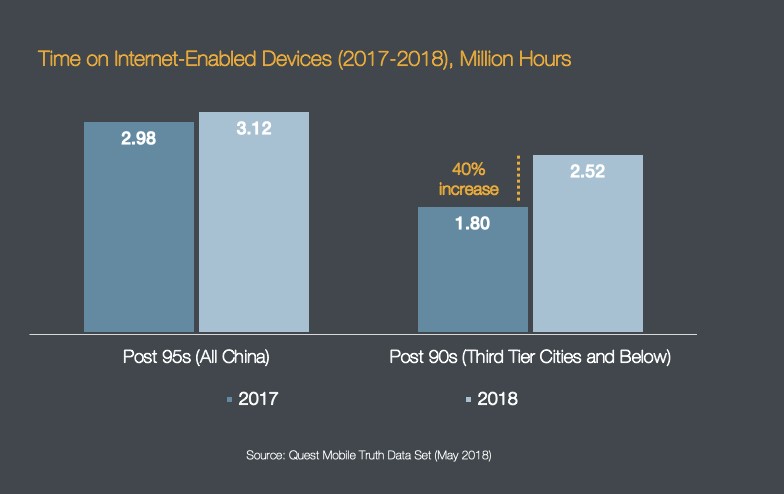

The time on device dividend is still in play, but will weaken soon. China’s internet users spent an average of 27 hours a week on mobile devices in 2017. In aggregate, that figure isn’t really going anywhere. The total time Chinese internet users spent on mobile internet increased by around 8 minutes between 2016 and 2017.

Of course, there’s variance by age and geography. Much of the growth in time online is now coming from millennials in China’s third, fourth and fifth-tier cities.

Figure 2: Breakdown of Time on Device Increases Among Millennials and Millennials from Third-Tier and Below Cities

Outside those smaller cities, it’s a zero-sum game for attention and traffic between China’s competing consumer-facing platforms, apps, and digital services.

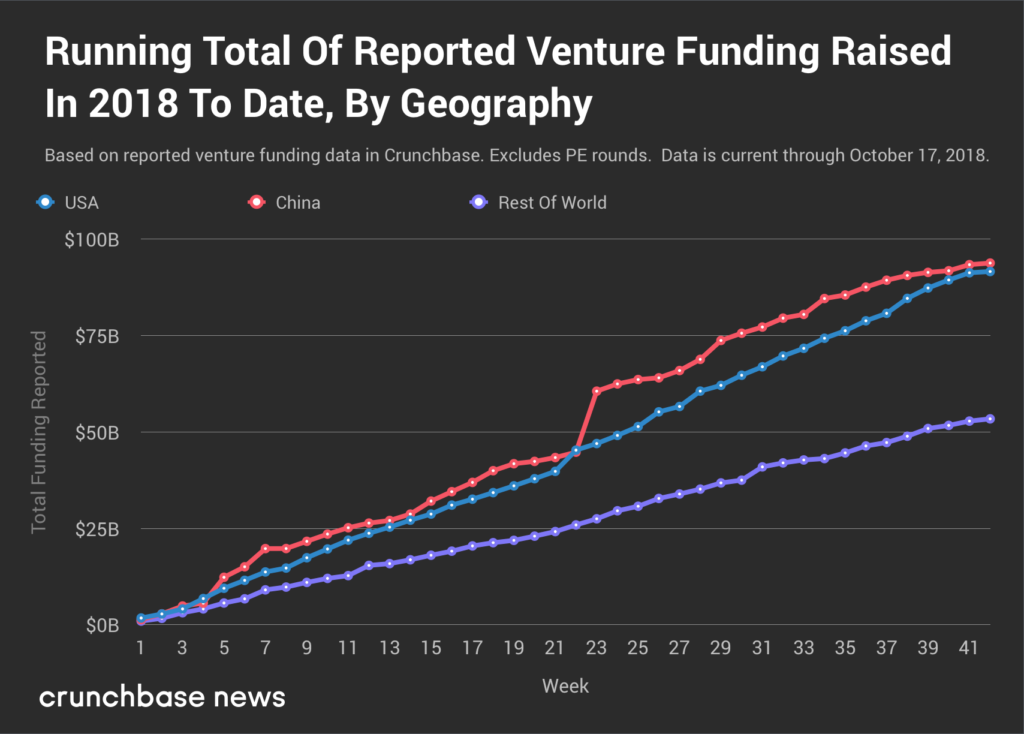

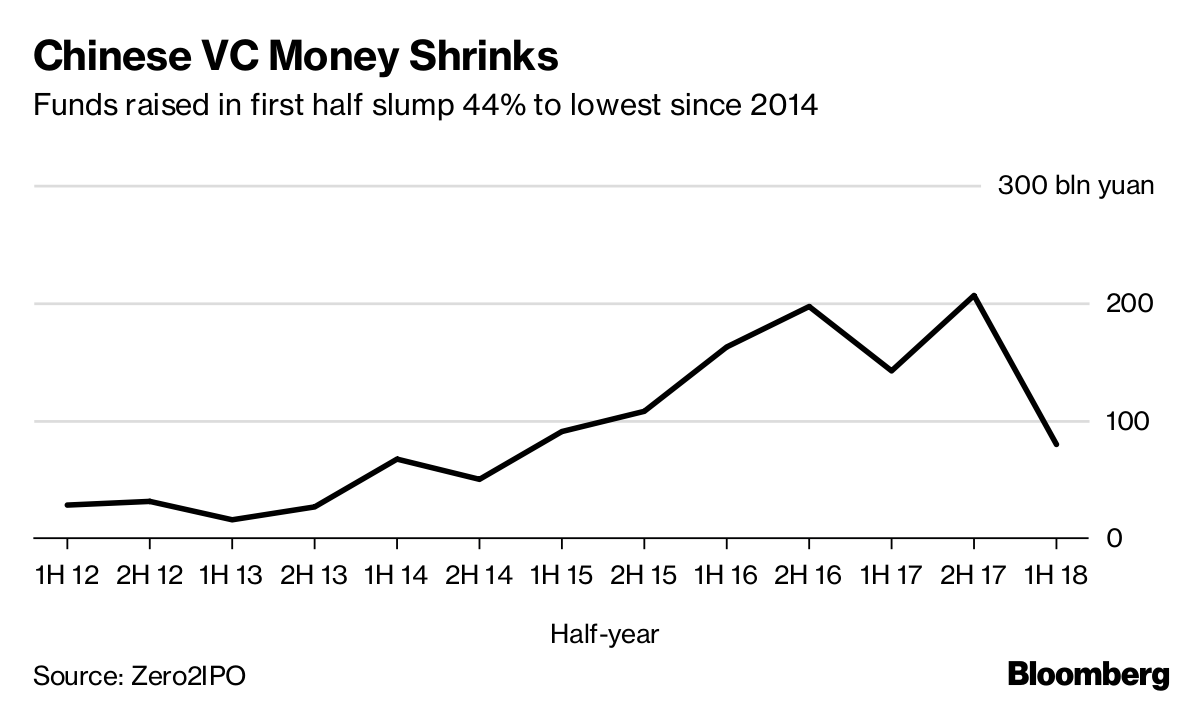

Firstly, capital upturns and downturns are cyclical. If there is a downturn, it may only be temporary. Secondly, there are mixed signals as to whether there’s more or less fundraising activity in China.

On the one hand, China now attracts more than a third of the world’s venture capital. It’s reported that last year China’s startup and tech scene gained more funding than all other countries, including the US.

But, on the other hand, it’s also reported China’s venture capital scene is in the middle of a cash crunch. It’s claimed China’s venture capital firms registered more than 50% fewer new funds and raised 70% less in Q3 2018 than in Q3 2017.

I’ve borrowed graphs that show the two different narratives below.

Figures 3 and 4: A Tale of Two Funding Stories

II. Wang Xing’s “The End of the Beginning” (互联网下半场) recognizes the end of fast, cheap user growth creates new pressures

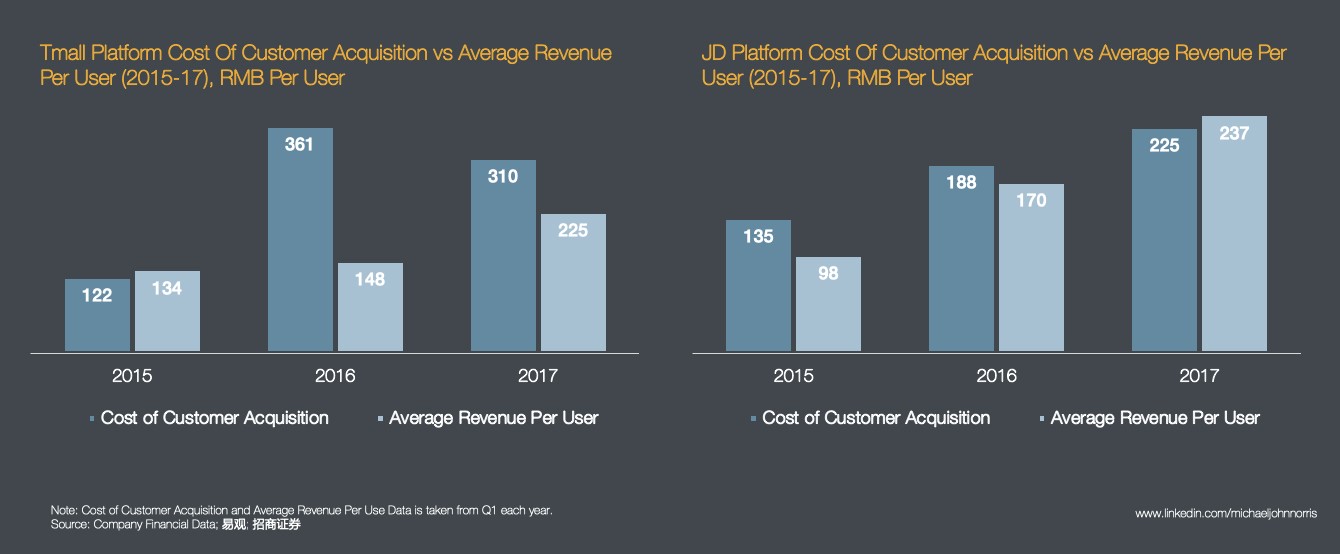

Figure 5: Tmall and JD’s Cost of Customer Acquisition and Average Revenue Per User

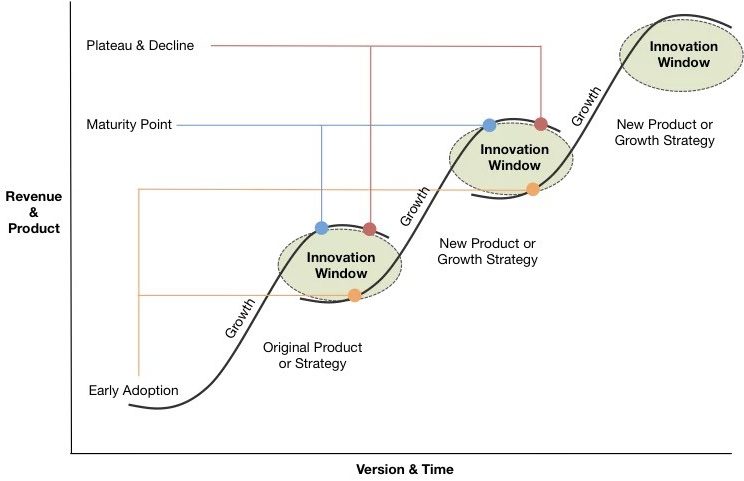

As a result of slower growth and higher costs, Wang Xing proposed that China’s internet landscape had entered互联网下半场. 互联网下半场 and Ben Evan’s “The End of the Beginning”, refer to the same point on the technology S-curve – where the market reaches relative maturity after rapid growth.

Figure 6: Technology S-Curves

This has a couple of implications. First, the prohibitive cost of acquiring users fortifies established platforms with large user bases. Pinching market share from existing services requires buckets of cash. And, if funding conditions in China are indeed taking a turn, the requisite cash needed is going to be harder to accrue.

Second, under-developed commercial models are going to be tested. Without a high-margin service that effectively cross-subsidizes user acquisition and engagement, digital businesses are at the mercy of their investors’ patience.

Lastly, it should be clear that users are digital companies’ most valuable resource. Working off a slightly tired cliché, if data’s the new oil, then user traffic is an oil field.

III. The end of fast, cheap user growth isn’t a China-specific phenomenon

At this point, it’s worth noting “The End of the Beginning” isn’t a China-specific phenomenon. Mary Meeker, Ben Evans and others observe that close to three-quarters of adults on the planet now have a smartphone, and half of the world’s population is connected to the internet. Here’s what Mary Meeker said on the topic last year:

“Growth continues to slow. Global smartphone new smartphone unit shipments had zero percent growth in 2017 versus two percent growth in 2016. Internet users, slowing growth of seven percent versus 12 percent growth in the previous year. Global internet users of 3.6 billion surpassed half the world’s population in 2018.

The reality of all that for the business people in the room, when you get to a market, when you get to 50 percent penetration, new growth becomes a lot harder to find.”

Accordingly, the ‘meta-questions’ tech companies across Silicon Valley, Shenzhen, Bangalore and Berlin face are fairly similar:

- What white space is left?

- Is it possible to compete against GAFA or BATTMD?[2]

- Where’s the next big growth opportunity after the mobile internet?

[2] GAFA refers to Google, Apple, Facebook, Amazon; BATTMD refers to Baidu, Alibaba, Tencent, Toutiao (Bytedance), Meituan and Didi.

IV. The end of fast, cheap user growth doesn’t mean no growth

In relation to the first question – what white space is left – China’s internet ecosystem still has some (relatively) fast, (relatively) cheap growth in the tank.

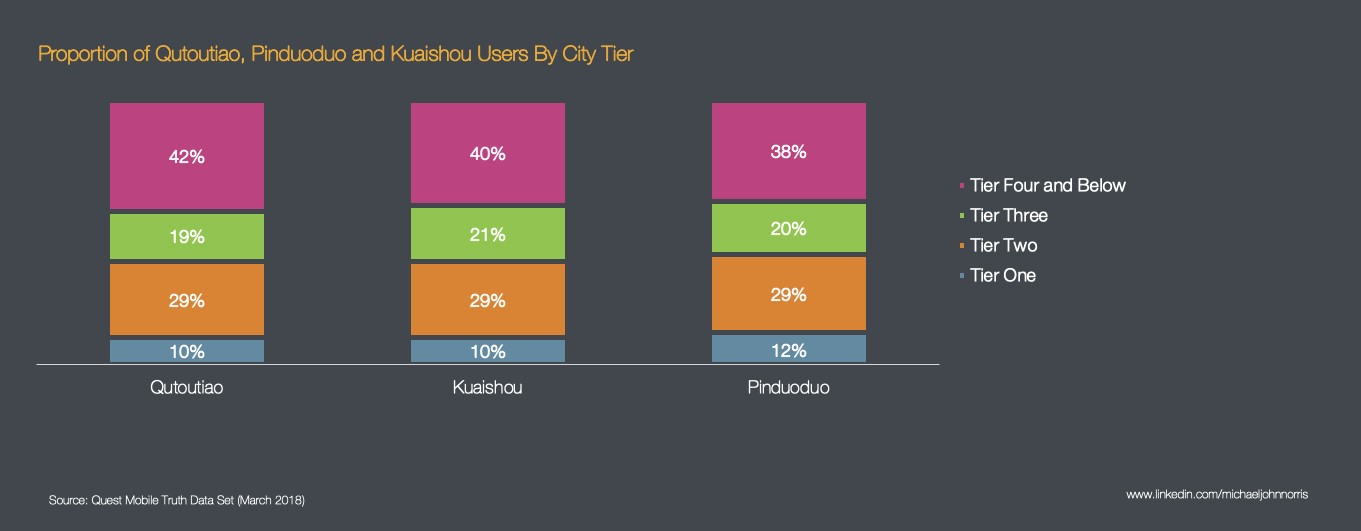

China’s new and new-ish internet users, often from smaller cities, are still forming digital habits. This means more time online, as well as decisions on where and how to spend time online. It’s this group that’s formed the backbone of short video and group-buying user bases.

Figure 7: Demographic Distribution of Select Short Video, Group-Buying and News Reading Apps

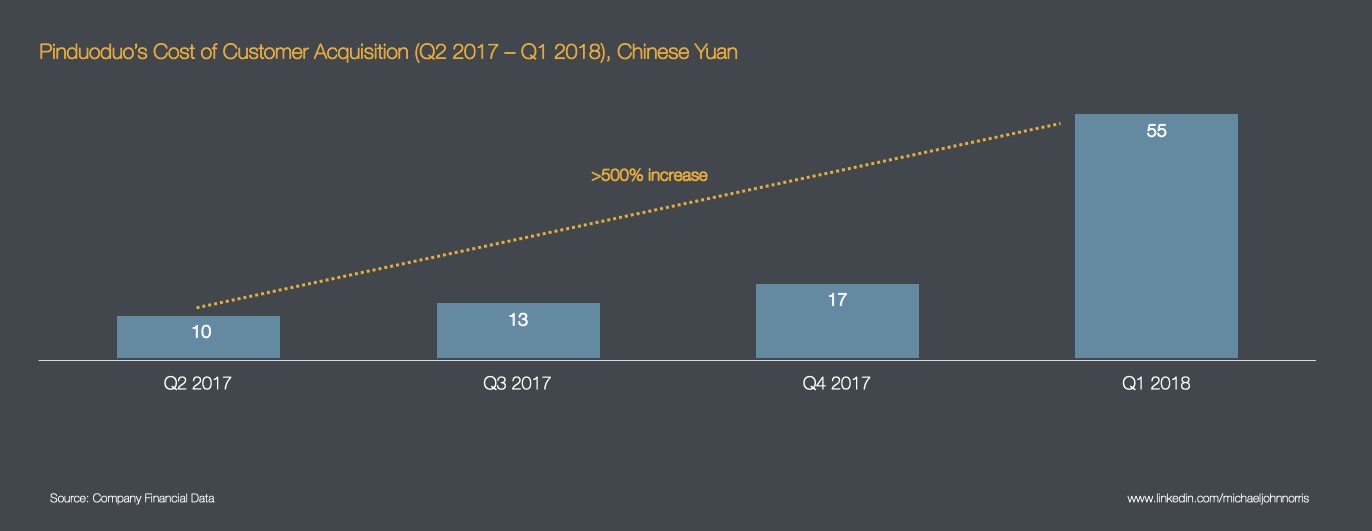

And, as Pinduoduo’s cost of customer acquisition data shows, gaining this group’s attention was relatively inexpensive – at least in the beginning.

Figure 8: Pinduoduo’s Cost of Customer Acquisition

This has prompted incumbents and challengers to explore 下沉 growth strategies, which focus on acquiring new users from China’s populous but unevenly-developed third, fourth, fifth and sixth-tier cities.

Yet, as Pinduoduo’s customer acquisition costs show, there’s a limit to cheap growth in third, fourth, fifth and sixth-tier cities. Apps, platforms and services focused on smaller cities will eventually face the same challenges – higher acquisition costs which probably eclipse user revenue.

2. China’s economic growth is slowing

Further complicating “The End of the Beginning” is worsening macroeconomic conditions. This places further pressure on growth trajectories and business models.

I’m very much underqualified to discuss economics generally, let alone the complexity that exists in China’s economy. Accordingly, this section will be brief and factual.

I. There are various indications of an economic slowdown

There are various indications of economic slowdown, across GDP growth, factory activity, stock market performance, and consumer spending.

Between July and September 2018, China’s GDP increased at the slowest rate since 2009. China’s GDP growth target for 2018 was 6.5%, and it’s rumored 2019’s growth target will be around 6 percent. The World Bank and International Monetary Fund have each revised down their estimates for China’s economic growth over 2019.

Factory activity is at its lowest level in two years. New factory orders have also decreased, suggesting factory activity won’t pick up in the immediate future.

China’s stock market has performed poorly. Shanghai’s stock index ended 2018 as the world’s worst market performer for a second year, falling 24.6 percent over 12 months.

There’s evidence consumers are tightening their belts. Car sales are down, property prices are sagging and retail growth is at its lowest level in more than 15 years. Wang Bin, a Ministry of Commerce official, projects domestic consumption will contribute two-thirds of China’s GDP in 2019, down from three-quarters in 2018.

II. The Chinese government, academia, and business have reached some level of consensus around the slowdown’s existence

Chinese government, academia, and business acknowledge the economic slowdown’s existence. However, these groups differ in their assessment of China’s vulnerability to further and persistent downturn.

China’s policymakers have acknowledged China’s economy faces downward pressures and an increasingly challenging external environment.

China’s academics have pointed out structural and non-structural issues affecting China’s economy, which include trade tensions with the United States, debt, a declining private sector economy, and the RMB’s valuation.

Private business has openly acknowledged economic slowdown’s impact on present and forecasted business performance. Deloitte’s Quarterly China CFO Survey indicates 82% of CFO respondents were less optimistic about China’s economic prospects than six months ago.

e-Commerce giants Alibaba and JD believe softening consumer spending led to reduced Gross Merchandise Volume growth over 2018’s Singles Day Sales.

3. As “The End of the Beginning” and slowing economic growth collide, major players are orienting themselves towards new growth

Although “The End of the Beginning” and economic headwinds pose their challenges, I think there are clear bright spots for future growth. I also think it’s now pretty clear where Baidu, Alibaba, Tencent, Toutiao, Meituan, Didi, Pinduoduo and JD are placing their bets.

I. There are clear future growth ‘swim lanes’

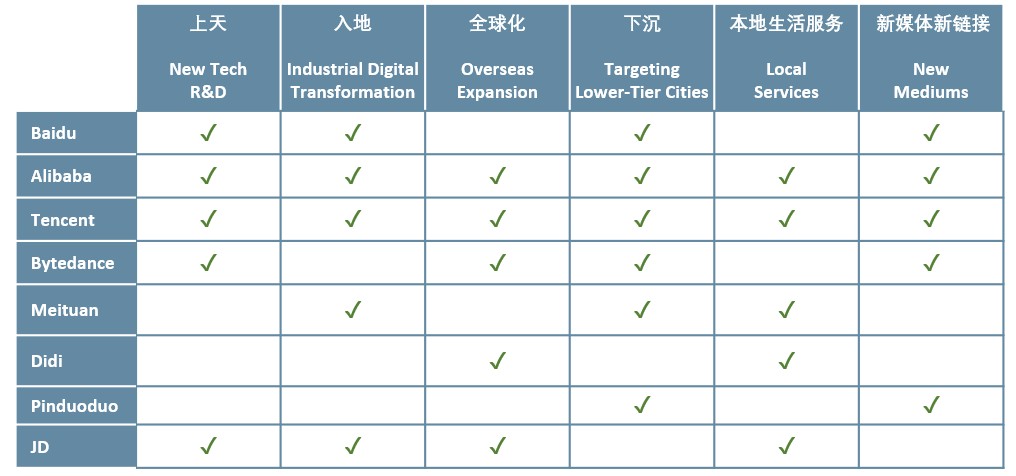

After Wang Xing proposed “The End of the Beginning”, he saw three strategic directions firms could take (互联网下半场的三个方向):

- “上天”, investment in and deployment of technological assets like cloud storage, machine learning and big data analytics

- “入地”, digital transformation across industry and service sectors, such as Alibaba’s New Retail or Meituan’s back-end for restaurants

- “全球化”, Chinese companies taking products to developed and developing markets, like Ant Financial’s international expansion or Bytedance exporting and localizing Douyin for international markets

I’d add another three:

- “下沉”, using existing products to capture attention-share and wallet-share of internet users in smaller cities or rural populations, or designing products and services exclusively for these groups

- “本地生活服务”, where digital giants go it alone and reshape markets, such as mobility, delivery, housing rental, and health

- “新媒体,新链接”, using existing and new technology to create new value propositions, interesting digital experiences and new mediums, like short video’s combination with e-commerce or gamified reading systems

In total, we’ve got six broad directions that major players Baidu, Alibaba, Tencent, Toutiao, Meituan, Didi, Pinduoduo and JD can move in to shape digital behavior, compete for white space, transform industries and race toward the next biggest growth opportunity after the mobile internet.

One of the truly interesting things about “The End of the Beginning” is the interplay between the post-digital and pre-digital economy, and whether distinctions like ‘pre-digital’ and ‘post-digital’ even matter anymore. As Tom Goodwin put it:

“The world’s largest taxi firm, Uber, is buying cars. The world’s most popular media company, Facebook, now commissions content. The world’s most valuable retailer is now Amazon, and has more than 350 stores. And the world’s largest hospitality provider, Airbnb, increasingly owns real estate. Things change.

Before, these companies were praised for the genius of building a thin layer of horizontal services on top of massive businesses with fixed assets. They added value to vast audiences with relatively few staff and no assets. What we now see is how they’ve had to build foundations, offer more services and add depth to their offering — these companies have moved from facades to edifices.”

II. Major players have pretty much settled on their ‘swim lanes’

Although it looks frenetic at times, China’s leading tech players know where they’re going for future growth.

Over 2017 and 2018, a number of key players restructured to strengthen core business offerings and better orient themselves to future growth opportunities. Most restructures were also accompanied by instructive visions about where future strategy is headed.

When you take that information and map the big players across the six growth buckets above, you get a fairly good sense of who’s competing where for future growth.

Table 1: Matrix of Major Players and Growth Strategies

About The Dispatch’s Author

Michael Norris is presently Strategy and Research Manager at AgencyChina. He’s delivered breakthrough insights, analysis and strategy to local and international brands, including Nestle, JD Toplife, Harbin Beer, Unilever, Shell and Tiffany. Michael is also one of the most dynamic commentators on China’s digital, social and business landscape. You can find more of Michael’s commentary on LinkedIn. Michael Norris |